In 2026, the global solar PV industry is approaching a critical development inflection point. After years of continuous capacity expansion and periodic oversupply, the industry is gradually leaving behind the era of scale competition — where rankings were determined purely by shipment volumes. As trade rules such as the UFLPA and the EU Carbon Border Adjustment Mechanism (CBAM) become increasingly normalized, and as N-type technology iteration enters its mid-to-late phase, the core competitive logic of the global PV industry has undergone a fundamental transformation.

Recently, third-party research firm Terawatt PV Research published its inaugural Terawatt PV 100 ranking, covering the full PV supply chain — polysilicon, wafers, cells, modules, and auxiliary materials — providing a concrete illustration of this industry transformation. The results show that scale advantage alone is no longer a sufficient guarantee of market position; full supply chain integration, financial and operational resilience, and supply chain compliance and transparency are emerging as the three core competencies that enable PV companies to navigate industry cycles.

A Reconstructed Evaluation Framework: From "Scale Supremacy" to "All-Round Competition"

For a long time, module shipment volume was the primary metric for measuring company strength in the PV industry. However, during a period of deep industry adjustment, a single metric can no longer fully reflect comprehensive competitiveness. The launch of the Terawatt PV 100 marks a shift in industry evaluation from an emphasis on scale expansion toward a holistic assessment that also weighs industrial ecosystem health and long-term value creation.

In the full supply chain dimension, vertical integration is no longer simply a matter of stacking capacity; it is a comprehensive test of capacity balance across segments, supply chain coordination efficiency, and cost management capability.

On the financial front, the ranking de-emphasizes short-term net profit performance and instead focuses on operating cash flow and debt structure health. Against a backdrop of relentlessly intense price competition, cash flow robustness directly determines a company's ability to withstand cyclical risks, and is the key factor in the concentration of competitive advantage during the industry shakeout.

In terms of compliance and transparency, ESG disclosure and supply chain traceability have shifted in 2026 from optional bonus items to hard prerequisites for accessing high-premium European and American markets. A company's compliance score directly affects its overseas financing costs and project bidding eligibility, constituting a critical soft-power barrier to global operations.

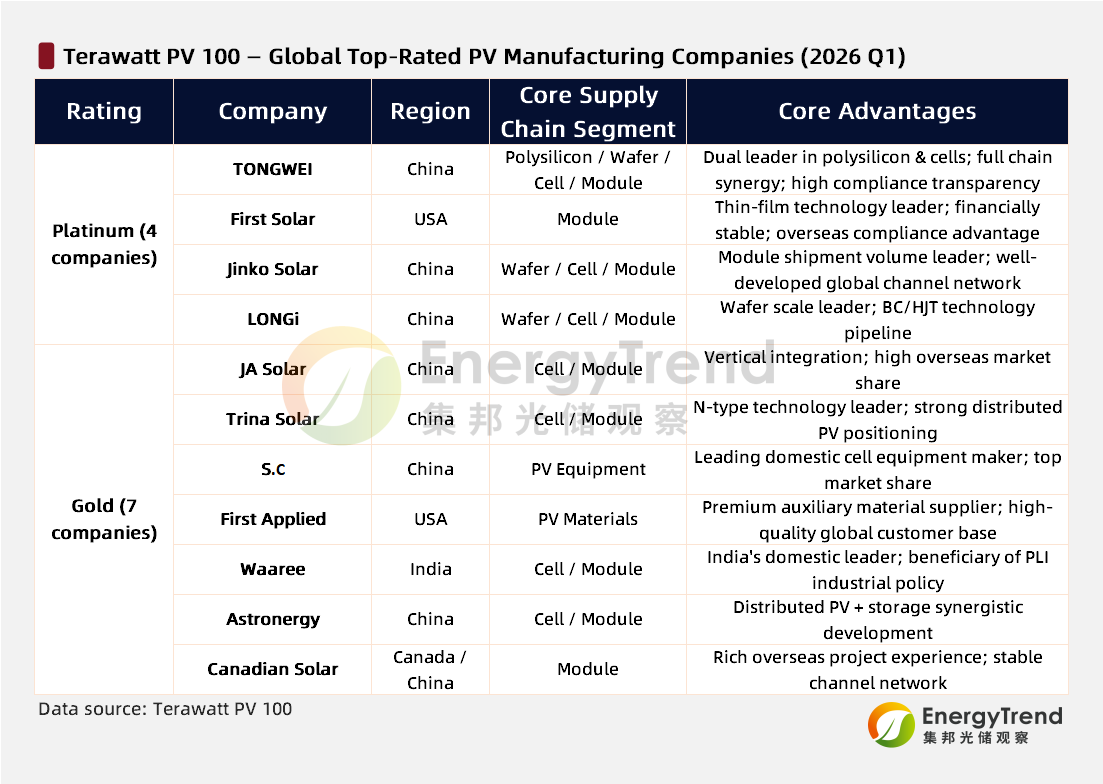

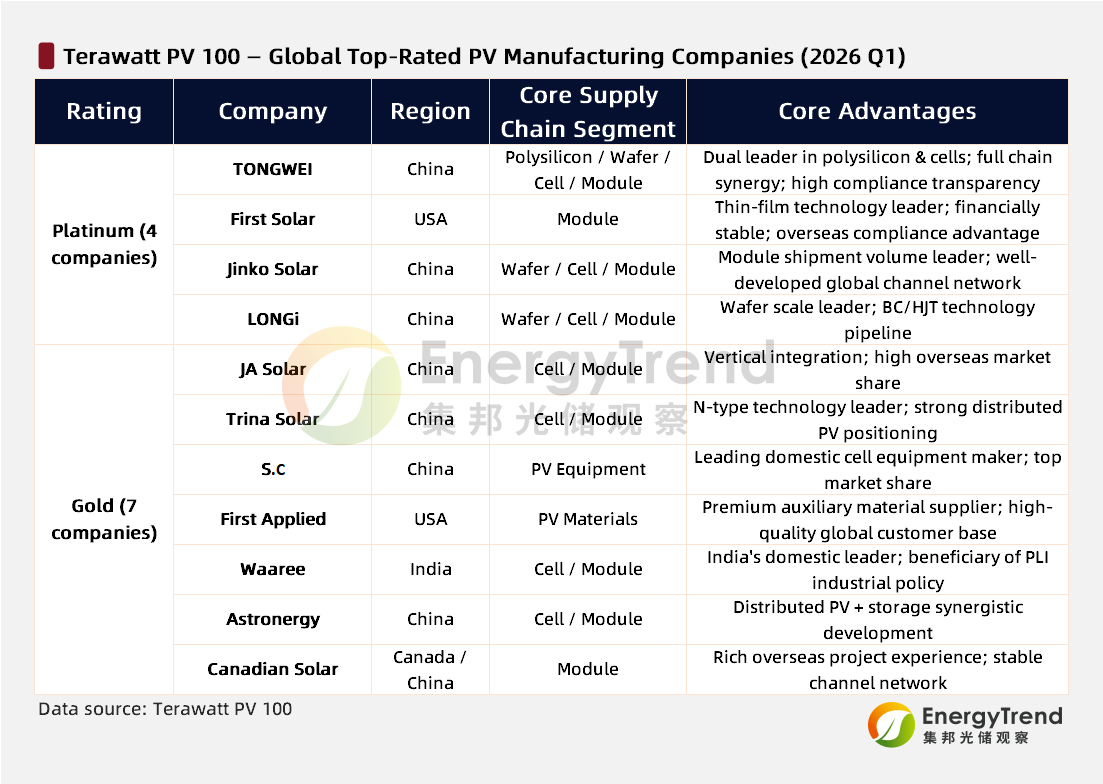

Reading the Rankings: Tongwei Tops the List; Chinese Companies Shift from "Big" to "Strong"

In the Terawatt PV 100, TONGWEI topped the rankings on the strength of its comprehensive full supply chain integration and outstanding financial resilience, earning the highest Platinum rating alongside First Solar, LONGi Green Energy, and Jinko Solar. This result reflects both individual corporate strength and the broader transformation of China's PV industry from scale leadership to quality leadership — with technology innovation as the core pillar underpinning Tongwei's competitive advantage and driving industry upgrading.

On the technology front, Tongwei's TNC 3.0 module leverages a quad-cut circuit design, louvre-style interconnection, and 360° surface passivation technology to achieve mass-production cell efficiencies of up to 26.3%, with G12-66 large-format modules reaching a peak power output of 770 W — fully aligned with the industry's trend toward larger formats and higher efficiency.

According to TrendForce estimates, the N-type cell market penetration rate will continue to rise in 2026; by end-2026, N-type cell capacity share is projected to reach 94%, with output share surging to 97%, firmly establishing N-type as the absolute mainstream. This technological dividend is highly consistent with the industry's "larger format, higher efficiency" development trajectory, suggesting that Tongwei's technology roadmap is precisely timed to coincide with the industry's next inflection point.

Figure: Terawatt PV 100 Ranking

Figure: Terawatt PV 100 Ranking

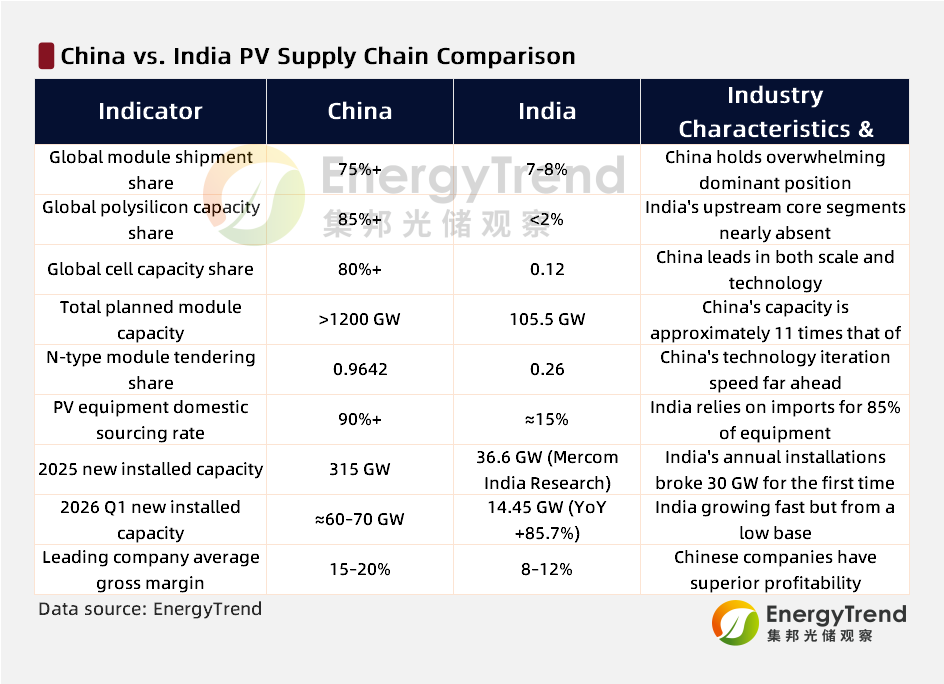

Global Manufacturing Map Shift: Chinese Companies Dominate, India Rises

The Terawatt PV 100 also reveals the physical repositioning of the global manufacturing map. TrendForce data shows that while China's PV supply chain capacity across all segments still exceeds 80% of global share in 2025, variables are emerging — with the overall picture now characterized by "Chinese dominance, Indian pursuit, and tiered divergence."

From the perspective of Chinese company rankings, China's dominant position remains intact. Chinese companies account for approximately 60% of the Top 100, occupying 8 of the top 10 positions; the completeness of China's manufacturing ecosystem is irreplaceable in the near term.

Indian companies' rankings have become an important variable. Driven by the PLI (Production-Linked Incentive) scheme, 21 Indian companies entered the Top 100, with Waaree breaking into the global top ten. Although most Indian companies currently sit in the Silver and Bronze tiers — with gaps in technology reserves and financial resilience relative to the top players — their rapid domestic capacity expansion has already posed a real challenge to Chinese companies' market share in Southeast Asia, the Middle East, and other regional markets.

Figure: China vs. India PV Supply Chain Core Data Comparison

Industry Outlook: Technology Iteration and Compliance Upgrade

Standing at the 2026 inflection point, the global PV industry presents both opportunity and risk. TrendForce identifies three major industry trends.

On capacity: current global module capacity exceeds 1,200 GW against annual market demand of approximately 600 GW, implying a capacity utilization rate below 50%. TrendForce projects that between 2026 and 2027, the elimination of legacy capacity will accelerate, with approximately 15–25% of inefficient capacity potentially being retired, and market share continuing to concentrate toward financially healthy, compliance-capable leading producers.

On technology iteration: TOPCon cells, with a market share exceeding 50%, remain the current mainstream technology; BC technology is gradually gaining penetration in the distributed PV segment; HJT technology is advancing in parallel; perovskite tandem cell laboratory efficiency has broken through 33%; and the industry technology iteration cycle has compressed to 2–3 years.

Notably, supply chain compliance has become an "invisible tariff." As European and American trade policies and carbon barriers continue to tighten, supply chain transparency has shifted from "optional" to "standard requirement" — companies unable to demonstrate traceability will face escalating overseas operational risk and cost pressures.

Conclusion

The second half of the PV industry's story is unquestionably a comprehensive contest of technology, resilience, and transparency. The Terawatt PV 100 defines what it means to compete in the all-round era: technology leadership is the admission ticket; scale advantage is the ballast; financial robustness is the life preserver; and compliance transparency is the passport.

The Platinum-tier Chinese companies led by Tongwei — through sustained R&D investment and disciplined operational management — are consolidating their advantages through this industry cycle adjustment. Looking ahead, PV manufacturers with full supply chain competitiveness, financial health, and compliance transparency will emerge as the core pillars of the global energy transition.